Modern Council Payments: What UK Citizens Expect, and Where Current Systems Fall Short

Published on: May 15, 2026

Insights from a national study of 1,000+ UK residents, commissioned by HeyCentric in partnership with Stripe.

As UK local authorities move into 2026, financial pressure, digital expectations, and operational accountability remain closely linked. Payments, one of the most common interactions citizens have with their council, sit at the intersection of all three. Gaining a clear view of how citizens experience council payments today is essential to improving reliability, reducing friction, and supporting accessible, well-designed digital services.

New research into council payment behaviours among citizens whose payments are not fully automated shows that while digital payments are now the norm, the overall payment experience has not always kept pace with citizen expectations, creating friction for users and operational challenges for councils.

Below, we explore key insights from the data and what they mean for the future of council income management.

Digital channels are the default for council payments

How citizens prefer to pay their council is now clear. The vast majority favour digitally managed payment channels, with direct debit (36%) and online payments via council websites (33%) leading by a wide margin. A further 17% prefer bank transfer or standing order.

Traditional channels now play a minimal role in payment preference, with only 4% of citizens choosing to pay by phone, 4% preferring to pay in person, and less than 1% preferring to pay by mail.

Digital wallet use remains limited overall (3%), but preference is higher among younger citizens. Among those aged 18-29, 7% prefer digital wallets, while fewer choose in-person (2%) or phone payments (3%). This signals potential growth in digital wallet adoption over time, alongside continued decline in traditional methods.

What this tells us

Citizens overwhelmingly prefer remote, digital-first payment channels for council services. Phone and in-person payments now represent a very small minority of preferred behaviours. This is not an emerging trend, it is an established baseline.

Why it matters

Payments are among the most frequent touchpoints between citizens and their council, and councils have a duty to provide multiple, convenient payment options that meet the needs of all citizens, including people with disabilities. As digital channels become the norm, reliability, clarity, and ease of use are no longer optional enhancements. They are central to effective service delivery and essential to keeping services accessible, inclusive, and barrier-free.

Convenience and ease of use are the strongest drivers of payment preference

When asked why they prefer a particular way of paying their council, citizens consistently prioritise convenience and ease of use above all other factors. Nearly half cite convenience (48%) and ease of use (46%) as key drivers of their payment preference, ahead of considerations such as trust and security (27%) or the ability to track payments (26%).

By comparison, financial incentives play a much smaller role. Fewer than one in five cite low or no fees (18%), and even fewer point to avoiding late fees (8%) or rewards and cashback (9%) as important factors.

What this tells us

Payment preference is driven primarily by convenience and ease of use, rather than incentives or penalties. This highlights the importance of payment experiences that are simple, predictable, and efficient.

Why it matters

For councils, improving payment outcomes is about designing high-quality payment journeys. Clear flows, intuitive interfaces, and dependable execution reduce friction at the point of payment and support timely completion without additional enforcement. Investing in experience quality enables councils to address citizen needs proactively and positively, while reducing dependence on fees or reminders and minimising avoidable operational strain.

Reasons For Payment Preference:

Process reliability affects payment completion

50% of respondents report having experienced issues with the online payment experience.

Among those who encountered problems, the most commonly reported issues were technical or usability-related, including technical glitches (41%), slow website performance (41%), and lack of simplicity (34%).

More than 1 in 3 citizens report abandoning an online payment due to a problem, most often for the following reasons:

- Technical failures (70%)

- Device or browser issues (30%)

- Payment journeys that felt too slow or complicated (27%)

These same issues appear again when looking at why citizens abandon payments altogether.

What this tells us

The overlap between these findings is clear. Technical instability, poor performance, and complex or unclear payment journeys are the issues citizens most frequently encounter online, and they closely align with the circumstances in which payments are most likely to be abandoned. While not every issue leads to non-completion, the data indicates that when these specific problems occur, the likelihood of abandonment increases.

Why it matters

Even when experienced by a subset of users, process issues can have a disproportionate impact. Failed or unclear payments often lead to repeat attempts, increased contact-centre demand, delayed income, and reduced confidence in digital services. Focusing on technical reliability, speed, and simplicity within online payment journeys helps reduce friction at critical moments, improving accessibility, convenience, and potentially increasing collection rates.

Online Challenges When Paying Council (among those who experienced issues):

Beyond improving reliability, the findings suggest that councils can further improve convenience by reducing repeated actions across payment journeys.

Opt-in appetite exists for saved payment information

A meaningful share of citizens are open to councils securely saving payment information for future use: 41% of citizens say they would be likely to use a service that allows their council to securely save payment details.

What this tells us

This points to demand for reduced repetition in council payments, supporting faster repeat payments and, where appropriate, enabling recurring arrangements.

Why it matters

Secure saved-payment functionality offers a way to improve repeat experiences without requiring full automation for every user or every payment type.

Automation improves satisfaction, but manual digital journeys still matter

We found that 26% of citizens do not have their monthly council payments fully automated; within this group, half make some automated payments, while the other half rely entirely on manual payments. Even partial use of automation correlates with higher satisfaction: 74% of citizens who make some automated payments report being very or somewhat satisfied, versus 58% of citizens whose payments are wholly manual, a 16-point increase.

However, lower satisfaction among the wholly manual group does not translate into greater demand for automated payments. Instead, their preferences skew toward manual digital payment methods:

- 49% prefer paying online via the council website (compared with 33% overall)

- Only 16% prefer direct debit (versus 36% overall)

An income pattern is also evident, with 68% of respondents earning under £29k reporting no automated payments.

What this tells us

Automation is the dominant payment model today, and it is associated with higher satisfaction, suggesting it can improve the experience for citizens who opt into it. However, a meaningful minority of citizens continue to rely on non-automated digital payments, favouring manual, one-off transactions that offer greater control. Taken together, these findings suggest that non-use of automation is associated with different payment preferences and circumstances.

Why it matters

For councils, this highlights the importance of supporting both automated and non-automated digital journeys. Automation can improve outcomes for some users, but reliable, simple manual payment experiences remain essential, particularly for households that may prefer flexibility or tighter control over payments.

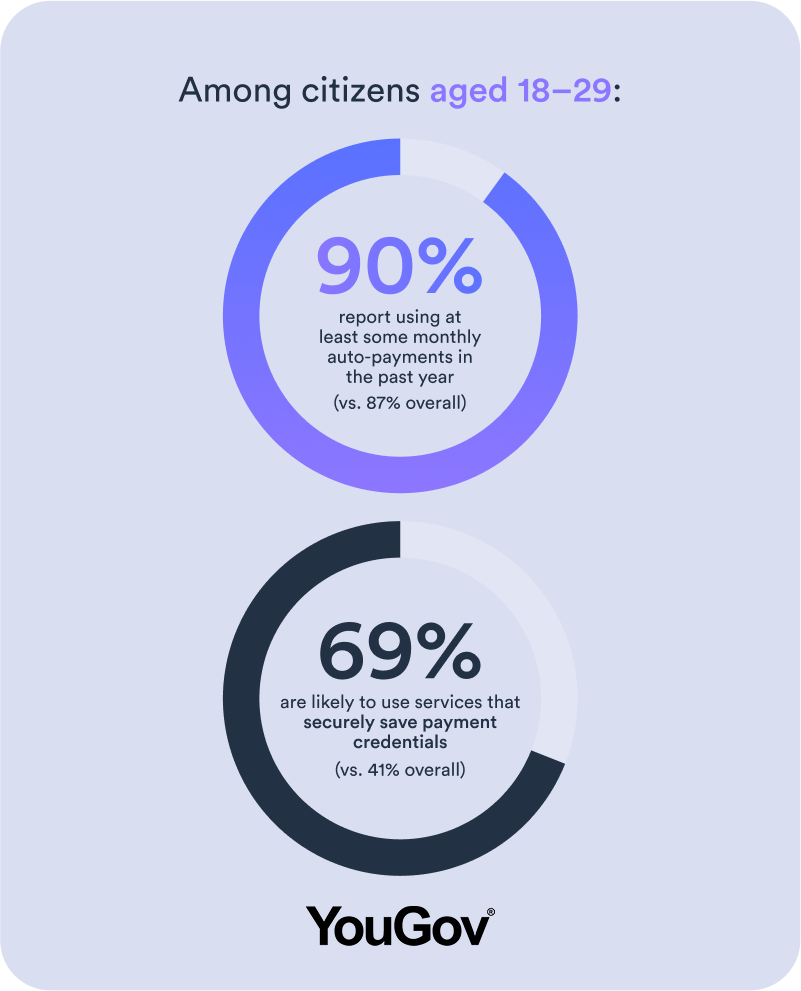

Younger citizens signal where expectations are heading

Among younger citizens aged 18-29, payment behaviour reflects a stronger orientation toward ease and automation:

- 69% say they are likely to use services that securely save payment credentials (compared with 41% overall)

- 90% report using at least some monthly auto-payments in the past year (compared with 87% overall)

What this tells us

Younger citizens are already comfortable with automated, credential-based, and mobile-first payment interactions. Their preferences are not outliers; they reflect behaviours that are becoming normalised earlier in adulthood and are likely to persist over time. The data points to rising expectations around reduced repetition, fewer manual steps, and payment journeys that improve with continued use.

Why it matters

As younger cohorts become a larger share of council service users, expectations shaped by everyday digital experiences will increasingly influence perceptions of council services. Payment systems designed today need to support current behaviours, while remaining flexible enough to accommodate greater use of automation, saved credentials, and mobile-first interactions in the future.

Designing council payments for the way citizens want to pay

Taken together, the data shows that digital payments are firmly established, automation improves outcomes for some, and reliability and ease of use remain the most critical levers. The opportunity for councils lies in strengthening digital payment journeys today, while enabling automation where it adds value.

That's where HeyCentric, powered by Stripe, comes in.

HeyCentric's income management platform is purpose-built for the public sector, combining:

-

Simple, intuitive payment journeys for citizens

-

Secure, compliant handling of payments and saved credentials

-

Powerful integration, reconciliation, and reporting tools for finance teams

-

Flexibility to support multiple payment methods, including secure recurring payments via cards and UK Direct Debit

With Stripe's secure, scalable payments infrastructure at its core, HeyCentric helps councils collect income more reliably, reduce operational strain, and deliver a better experience for every user, without compromising on governance or control.

Modernise income collection with confidence.

If your council is re-evaluating its approach to income collection, now is the time to modernise with confidence. See how HeyCentric, powered by Stripe, helps councils modernise income collection: improving reliability, reducing friction, and supporting the way citizens want to pay.